1. Introduction

Banking business globally plays a significant role in the economic growth and development of a nation. The economic growth of any nation is driven by the banking sector as the most critical sector as a result of its financial intermediation roles. Therefore, banks need to maintain stable performance to be relevant in performing their functions properly in smoothing the payment system, and in the implementation of monetary policy. The sector is also considered as the life blood of every nations; their issues may favorably or adversely affect the economy

| [1] | Adebola, F. T., Omuemu, S. O., & Babatunde, O. (2022). Capital Adequacy and Banks' Performance. Al-Hikmah International Journal of Finance (AHIJoF), 2(1), 1-11. |

| [2] | Ahana, S. (2021). IMPACT OF NPA ON BORROWERS: A STUDY ON SELECTED INDIAN PRIVATE SECTOR BANKS. International Journal of Advanced Research in Commerce, Management & Social Science (IJARCMSS), 4(1), 59-68. |

| [3] | Wahyuni, P., & Umam, D. (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12-28. https://doi.org/10.51505/IJEBMR.2023.7602 |

[1-3]

. Globally, financial system has faced significant challenges among which is financial sustainability which undermines the growth and development of various economies; developed and under-developed economies. Financial sustainability is key to organizational survival

| [4] | Gambo, N., Rikwentishe, R., Usman, N. D., & Ikyabo, A. Y. (2022). PROFITABILITY AND FINANCIAL SUSTAINABILITY OF MICROFINANCE BANKS IN NIGERIA. FUW-INTERNATIONAL JOURNAL OF MANAGEMENT AND SOCIAL SCIENCES, 7(2), 1-21. |

| [5] | Aliyu, A., Gambo, N., Enesi, O. E., & Ibrahim, M. (2023). Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria. European Journal of Accounting, Auditing and Finance Research, 11(10), 73-97. https://doi.org/10.37745/ejaafr.2013/vol11n107397 |

[4, 5]

.

In Europe, financial services sector is highly regulated and well respected in the whole world simply because of their stringent risk management, adequate financial disclosure requirements and corporate governance. However, despite the stringent regulations, the financial sustainability challenge still remains. Banks are closing down their branches and reducing their scales of operations because of their negative economic growth. Risk Assets are not growing and majority of the existing assets are not performing and consequently, banks’ capitals are getting eroded. In United State of America (USA), sustainability has become a widely accepted buzzword in both companies and society at large

. The state has experienced above seven banks’ collapsed in the year 2023 alone. All these collapsed banks negatively impacted US economy because of their multiplier effects; Loss of jobs, Lack of funds in financing Small and Medium Enterprises / Medium Scale Enterprises (SMEs / MSEs), Infrastructural Failure and so on.

In Africa, the economy of sub - Saharan African countries grew at the rates that match or surpass global rates. This improvement was evident in Egypt, Nigeria and South Africa and was made possible by the development and growth in the banking sector

| [7] | Capacity, B. M. (2022). An Independent Review of Multilateral Development Banks' Capital Adequacy Framework. World Bank. |

| [8] | Siyanbola, T. T., & Adebayo, K. K. (2021). Credit Risk Management and Financial Sustainability of Listed Deposit Money Banks in Nigeria. Journal of Research in Business and Management, 9(6), 64-77. |

[7, 8]

. Banking reforms in Ghana, Rwanda, Nigeria, South Africa, and Cote D’Ivoire have been designed to strengthen financial stability, enhance efficiency, and promote economic development. These reforms, while sharing common goals, have evolved based on the unique economic and regulatory environments of each country.

Siyanbola and Adebayo (2021) highlighted that Deposit Money Banks (DMBs) worldwide, including those in Sub-Sahara African countries

| [8] | Siyanbola, T. T., & Adebayo, K. K. (2021). Credit Risk Management and Financial Sustainability of Listed Deposit Money Banks in Nigeria. Journal of Research in Business and Management, 9(6), 64-77. |

[8]

, bear significant responsibilities in managing the risks associated with their banking operations while ensuring financial safety and sustainability. They encounter various risks that can undermine their financial stability and long-term growth, such as unexpected surges in loan defaults and arrears. Additionally, fraudulent loans initiated by their loan officers pose serious threats. Siyanbola and Adebayo (2021) opined that it is crucial for these banks to implement strong systems and procedures for risk identification, assessment, and prioritization, along with internal controls to prevent or detect undesirable outcomes

| [8] | Siyanbola, T. T., & Adebayo, K. K. (2021). Credit Risk Management and Financial Sustainability of Listed Deposit Money Banks in Nigeria. Journal of Research in Business and Management, 9(6), 64-77. |

[8]

. An efficient capital adequacy is a “significant area of an overall management capability because many businesses are directly dependent on external financing in the form of bank loans”

| [9] | Ogunode, O. A., Awoniyi, O. A., & Ajibade, A. T. (2022). Capital adequacy and corporate performance of non-financial firms: Empirical evidence from Nigeria. Cogent Business & Management, 9(1), 1-16. https://doi.org/10.1080/23311975.2022.2156089 |

[9]

.

As evidenced in Nigeria, South Africa, Ghana and major Sub-Sahara African countries, various reforms by governments and their agencies towards achieving financial sustainability did not produce the desired results. This in-effectiveness in achieving desired goals has led the regulators to focus more on capital adequacy as a critical tool in achieving financial sustainability. All over the world, capital adequacy is considered as one of the critical aspects that is regulated in many financial institutions. Capital adequacy is essentially used to measure bank’s financial health that indicates its ability to absorb potential losses and meet its other financial obligations

| [10] | Naoaj, M. (2023). Exploring the Determinants of Capital Adequacy in Commercial Banks: A Study of Bangladesh's Banking Sector. European Journal of Business and Management Research, 8(2), 108-112. https://doi.org/10.24018/ejbmr.2023.8.2.1887 |

[10]

. Although several regulatory reforms have been implemented in Ghana, Rwanda, Nigeria, South Africa, and Cote D’Ivoire including other sub-Sahara African countries towards strengthening financial sustainability and consequently; enhanced economies that are comparable to any developed economies. However, we are far from reaching the desired destinations and therefore not globally competitive. Enhanced capital adequacy is a common factor identified by the five countries in reaching their goals. Therefore, this study focused on “exploring the relationship between capital adequacy and financial performance of listed deposit money banks in selected sub-Sahara African countries”.

Listed deposit money banks are supposed to be financially sustainable in order to drive their growth rate and prevent future failure. Business sustainability enables corporate firms to sustain efficiency of operations and enhance intergenerational equity

| [11] | Sonkhaskar, J. D. (2020). A role of women globally in Environmental Protection. JOURNAL OF CRITICAL REVIEWS, 7(8), 2999-3008. |

[11]

. However, some DMBs in selected SSACs; Ghana, Rwanda, Nigeria, South Africa, and Cote D’Ivoire are still struggling to survive and be competitive in the global banking sectors due to poor financial performance as a result of poor return on equities. World Economic Forum in 2022 has identified different challenges facing sustainability in finance and investment in developing countries including sub-Sahara African countries amongst which are poor return on equity, poor return on assets, under capitalization and lack of sophisticated equipment. These challenges require urgent attention and strategic decisions in mitigating them. Return on equity (ROE) is a widely acceptable indicator in determining best businesses where shareholders can invest their limited resources and a good ROE should be at least 0.20. However, Nigeria, Rwanda, South Africa and Cote D’Ivoire listed deposit money banks’ average ROEs for the period 2014 to 2023 were 0.1385; 0.19325; 0.1495 and 0.176 respectively, while Ghana’s average ROE for their listed banks was 0.2288. The returns in Nigeria, South Africa and Cote D’Ivoire as indicated by their ROEs were poor returns while that of Rwanda was slightly below the globally acceptable ROE and generally affect the foreign funding of listed deposit money banks. Ghana’s ROE was considered fantastic at 0.2288.

Another major factor contributing to the financial performance in the listed DMBs in selected SSACs; Ghana, Rwanda, Nigeria, South Africa, and Cote D’Ivoire is poor return on assets (ROA). Banks’ major function is assets creation from deposits collected and in return earn their margins on those assets created. ROA is a profitability index employed by companies in ascertaining the efficient use of its assets. Any company that efficiently utilized its assets is expected to achieve higher ROA. We can also use it to determine if a company’s assets are under- utilized or over-utilized. It is considered under-utilized if its ROA is lower that the industry average ROA and over-utilized if it is higher than the industry average ROA. It shows the capacity of a firm in using its assets in generating profits. A good industry ROA should be between 5% - 20%. However, average ROAs for the listed deposit money banks in Ghana, Rwanda, Nigeria, South Africa, and Cote D’Ivoire for the period 2014 to 2023 were 2.4%; 2.7%; 1.6%; 2.23% and 2.16% respectively (Published Annual Reports, 2014 – 2023). These returns on assets as declared were generally below the global acceptable ROA of at least 5% and considered as a critical factor contributing to sustainability in the selected SSACs

| [8] | Siyanbola, T. T., & Adebayo, K. K. (2021). Credit Risk Management and Financial Sustainability of Listed Deposit Money Banks in Nigeria. Journal of Research in Business and Management, 9(6), 64-77. |

[8]

.

In addressing the above financial sustainability challenges in selected SSACs, effective capital adequacy measured by Deposit to Total Assets (DTA) as previously used by

; and

| [14] | Efuntade, A. O., Efuntade, O. O., & Akinola, A. O. (2019). Capital Structure and Earnings per Shares in Listed Conglomerates in Nigeria. European Journal of Accounting, Auditing and Finance Research, 7(8), 49 - 58. |

[14]

measures the “relative portion of the total assets that is funded by deposits and gives an informed analysis of the role of deposits as a funding source”. Loan to Total Assets (LTA) measures the proportion of the outstanding loans to Total Assets. It is a liquidity ratio that measures banks’ ability in meeting customers’ request for loans and advances against the banks’ Total Assets. Loan Loss Provision to Total Assets (LLPTA) is the proportion of loan provisions against the resources of the bank known as Total Assets. Generally, the lower the ratio; the better for the banks and the higher the profitability of the bank. It shows that management are in control of their risk assets and very compliant with the regulators’ directives; and lastly, Equity to Total Liabilities (ETL). ETL was earlier used by

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

| [21] | Sridevi, M. M., Sathyakala, S., Deepa, V., & Sabita, R. L. (2023). A Performance of Capital Adequacy Ratio Indicator in Private Sector Banks: An Empirical Study. BioGecko, 12(3), 2035-2046. https://www.researchgate.net/publication/372289332 |

[17, 21]

in their various studies. DER is the ratio of total debts to shareholders equity; the proportion of Shareholders’ Equity funds that owed the outsiders. This study empirically investigated the effect of capital adequacy on financial performance of listed DMBs in selected SSACs.

The main objective of the study is to examine the effect of Capital adequacy on financial performance of listed DMBs in selected SSACs while our specific objectives are to:

1. evaluate the effect of Capital Adequacy on Return on Equity of Listed DMBs in selected SSACs.

2. determine the effect of Capital Adequacy on Return on Assets of Listed DMBs in selected SSACs.

The following hypotheses developed, designed and stated in Null form were tested in the study at 0.05 level of significance:

Ho1: Capital adequacy has no significant effect on return on equity of listed deposit money banks in selected sub-Sahara African Countries.

Ho2: There is no significant effect of capital adequacy on return on assets of listed deposit money banks in selected sub-Sahara African Countries.

2. Literature Review / Theoretical Review

2.1. Conceptual Review

In this conceptual review, the study reviewed all variables as related to dependent and independent variables and their interrelationship.

2.1.1. Return on Equity

Return on Equity is defined by

| [15] | Gazi, M., Nahiduzzaman, M., Harymawan, I., Masud, A., & Dhar, B. (2022). Impact of COVID-19 on Financial Performance and Profitability of Banking Sector in Special Reference to Private Commercial Banks: Empirical Evidence from Bangladesh. Sustainability MDPI, 14, 1-23. https://doi.org/10.3390/su14106260 |

[15]

as the “standard of a bank’s profitability and how a bank can effectively generate profit from its employed equity. It is the ratio of return between a firm’s net income and its shareholders’ equity”. According to Nugrahani and Suwitho 2016 as cited by

| [16] | Marta, M. S., Gunawan, A., Maesaroh, S. S., Nugraha, & Bahri, S. (2022). Interactive Effect of Capital Structure on Profitability and Earning Per Share of Sharia Bank. Journal of Islamic Economics and Business, 2(2), 97-111. |

[16]

, ROE is a form of financial ratio that shows the company's ability to earn profits for the return on capital of shareholders. It therefore measures how effectively the capital provided by investors is managed by management (Shinta & Laksito, 2014) cited by

| [16] | Marta, M. S., Gunawan, A., Maesaroh, S. S., Nugraha, & Bahri, S. (2022). Interactive Effect of Capital Structure on Profitability and Earning Per Share of Sharia Bank. Journal of Islamic Economics and Business, 2(2), 97-111. |

[16]

. Return on Equity according to Agus (2010) as cited by

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

[17]

measures the ability of the company in obtaining profits available to shareholders of the company. ROE is a form of profitability ratio used to measure the amount of profit generated from Capital Investments issued. "Return on equity (ROE) is the ratio of net profit after tax to shareholders equity" (Furhmann, 2014) as cited by

| [18] | Mamun, M. A., Islam, H., & Sarker, N. K. (2022). Affiliation between Capital Adequacy and Performance of Banks in Bangladesh. Journal of Business Studies Pabna University of Science and Technology, 3(1), 155-168. https://doi.org/10.58753/jbspust.3.1.2022.10 |

[18]

. ROE is a measure of performance / earnings quality, explains the efficiency of using shareholders capital in the business. It is used to analyze the effect of decision-making in the achievement of perpetuity by company management on shareholder’s rate of return

| [19] | Aliyu, A. A., Abdullahi, N. A., & Bakare, T. O. (2020). Capital Adequacy and Financial Performance of Deposit Money Banks with International Authorization in Nigeria. International Accounting and Taxation Research Group, Faculty of Management Sciences, University of Benin, Benin City, Nigeria. Retrieved from http://www.atreview.org |

[19]

.

Return on Equity (ROE) measures the returns an investors derived in investing in the company. It measures returns of the company after all necessary expenses and tax against the Shareholders’ Equity. It simply means the return on every naira invested by the shareholders on the equity investment

| [20] | Kong, Y., Donkor, M., Musah, M., Nkyi, J. A., & Ampong, G. O. (2023). Capital Structure and Corporates Financial Sustainability: Evidence from Listed Non-Financial Entities in Ghana. Sustainability MDPI, 15(4211), 1-20. https://doi.org/10.3390/su15054211 |

| [21] | Sridevi, M. M., Sathyakala, S., Deepa, V., & Sabita, R. L. (2023). A Performance of Capital Adequacy Ratio Indicator in Private Sector Banks: An Empirical Study. BioGecko, 12(3), 2035-2046. https://www.researchgate.net/publication/372289332 |

[20, 21]

. It is net profit after tax (NPAT) over total equity; therefore all necessary expenditures including tax would have been taking into full consideration. The assumption here is that both the capital structure and tax rate remain the same throughout the year. It is very significant to the Equity Shareholders because all other financing costs like debts charges and costs of preference shares would have been recognized as part of the total company expenditures. ROE calculations by other earlier scholars are as stated below:

ROE = Profit after Tax / Total Equity

| [19] | Aliyu, A. A., Abdullahi, N. A., & Bakare, T. O. (2020). Capital Adequacy and Financial Performance of Deposit Money Banks with International Authorization in Nigeria. International Accounting and Taxation Research Group, Faculty of Management Sciences, University of Benin, Benin City, Nigeria. Retrieved from http://www.atreview.org |

[19]

.

ROE = Net Income after Tax/Shareholders Equity

| [15] | Gazi, M., Nahiduzzaman, M., Harymawan, I., Masud, A., & Dhar, B. (2022). Impact of COVID-19 on Financial Performance and Profitability of Banking Sector in Special Reference to Private Commercial Banks: Empirical Evidence from Bangladesh. Sustainability MDPI, 14, 1-23. https://doi.org/10.3390/su14106260 |

[15]

.

ROE = Net Income/Total Equity

| [20] | Kong, Y., Donkor, M., Musah, M., Nkyi, J. A., & Ampong, G. O. (2023). Capital Structure and Corporates Financial Sustainability: Evidence from Listed Non-Financial Entities in Ghana. Sustainability MDPI, 15(4211), 1-20. https://doi.org/10.3390/su15054211 |

[20]

.

In this study, ROE is defined as the proportion of Net Income to each unit of equity shares and calculated as stated below;

“Return on Equity (ROE) = Net Income / Average Total Equity”.

Several authors have considered the adapted ROE formula as the best measure of company’s performance valuation in peer review of firms in the same industry or comparison of current year performance with the prior year performance or benchmarking it with the analyst’s standard. Also, it is mostly used by investors in making appropriate investment decision; the higher the ROE, the better the company. Some prior authors that have used ROE as a dependent variables in their studies are:

| [5] | Aliyu, A., Gambo, N., Enesi, O. E., & Ibrahim, M. (2023). Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria. European Journal of Accounting, Auditing and Finance Research, 11(10), 73-97. https://doi.org/10.37745/ejaafr.2013/vol11n107397 |

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

| [20] | Kong, Y., Donkor, M., Musah, M., Nkyi, J. A., & Ampong, G. O. (2023). Capital Structure and Corporates Financial Sustainability: Evidence from Listed Non-Financial Entities in Ghana. Sustainability MDPI, 15(4211), 1-20. https://doi.org/10.3390/su15054211 |

| [21] | Sridevi, M. M., Sathyakala, S., Deepa, V., & Sabita, R. L. (2023). A Performance of Capital Adequacy Ratio Indicator in Private Sector Banks: An Empirical Study. BioGecko, 12(3), 2035-2046. https://www.researchgate.net/publication/372289332 |

| [51] | Joshua, A., Olweny, T., & Oloko, M. (2021). Influence of Credit Risk on Financial Performance of Deposit Taking Microfinance Banks in Kenya. International Journal of Academic Research in Accounting Finance and Management Sciences, 11(4), 82-98. https://doi.org/10.6007/IJARAFMS /v11-i4/11706 |

| [52] | Bawuah, I. (2024). Bank Stability and Economic Growth in Sub-Saharan Africa: Trade-offs or opportunities? And how do institutions and bank capital affect this trade-off? Cogent Economic and Finance, 12(1). https://doi.org/10.1080/23322039.2024.2381695 |

| [57] | Boateng, E., Antwi, J. K., & Abotsi, E. (2022). Bank Recapitalization and its impact on Ghana's Banking Sector Resilience. West African Economic Review, 22(2), 76-94. |

[5, 17, 20, 21, 51, 52, 57]

.

2.1.2. Return on Assets

Mamun et al. (2022) defined ROA as a “metric to measure the profitability performance. A bank's return on assets is higher when its balance sheet is managed to generate profits, but a lower ROA shows that there has been room for growth”

| [18] | Mamun, M. A., Islam, H., & Sarker, N. K. (2022). Affiliation between Capital Adequacy and Performance of Banks in Bangladesh. Journal of Business Studies Pabna University of Science and Technology, 3(1), 155-168. https://doi.org/10.58753/jbspust.3.1.2022.10 |

[18]

. "Return on asset is ratio of net profit after tax to total assets" (Hargrave, 2003) as cited by

| [18] | Mamun, M. A., Islam, H., & Sarker, N. K. (2022). Affiliation between Capital Adequacy and Performance of Banks in Bangladesh. Journal of Business Studies Pabna University of Science and Technology, 3(1), 155-168. https://doi.org/10.58753/jbspust.3.1.2022.10 |

[18]

. Return on assets (ROA) or asset withdrawal ratio, measures the relationship between pre-tax profits and total assets. This assessment provides a thorough understanding of the management's effectiveness in generating profits (Rivai, 2017) cited by

| [22] | Sapitri, N., & Irawan, B. (2023). Impact of the Capital Adequacy Ratio (CAR) and Mudharabah on the Return on Asset (ROA) on Sharia General Banks Registered in the Financial Services Authority (OJK). Journal of Waqf and Islamic Economic Philanthropy, 1(1), 1-12. |

[22]

. The Return on Assets (ROA) is a financial metric utilized to assess the efficiency with which a company utilizes its assets to generate profits. This ratio quantifies the profitability of the bank's entire management according to Sintiya (2018) as cited by

| [22] | Sapitri, N., & Irawan, B. (2023). Impact of the Capital Adequacy Ratio (CAR) and Mudharabah on the Return on Asset (ROA) on Sharia General Banks Registered in the Financial Services Authority (OJK). Journal of Waqf and Islamic Economic Philanthropy, 1(1), 1-12. |

[22]

.

Wahuyuni and Umam (2023) further defined ROA as a “ratio that shows the ability of all existing assets and their used in generating profits

| [3] | Wahyuni, P., & Umam, D. (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12-28. https://doi.org/10.51505/IJEBMR.2023.7602 |

[3]

. The reason for choosing ROA as a performance measure is because ROA is used to measure the company's effectiveness in generating profits by utilizing its assets”. If ROA has a high value, then the company's performance in managing assets to become a profit for the company is very good

| [3] | Wahyuni, P., & Umam, D. (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12-28. https://doi.org/10.51505/IJEBMR.2023.7602 |

[3]

. ROA indicates the revenue generated per unit of assets and replicates the bank manager's capability to utilize assets, investment capital and produce income. Higher levels of ROA signifies better profitability and performance, leading to an increased firm value

| [24] | Gathara, F., Mutwiri, N., & Aluoch, M. (2023). The Effect of Capital Adequacy on the Value of Commercial Banks in Kenya. International Journal of Business Management, Entrepreneurship and Innovation, 5(3), 55-69. https://doi.org/10.35942/92fcva46 |

[24]

. ROA is used to improve the ability of bank management in managing its activities to generate income (Ameliana, 2021) as cited by

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

[17]

. Return on Asset (ROA) can be used as a measure of financial performance

| [25] | Rafique, A., Quddoos, M., Akhtar, M., & Karim, A. (2020). Impact of Financial Risk on Financial Performance of Banks in Pakistan; the Mediating Role of Capital Adequacy Ratio. Journal of Accounting and Finance in Emerging Economies, 6(2), 607-613. |

[25]

.

ROA is a benefit proportion that demonstrates the organization's capacity to effectively create benefits from the all assets claimed. The more prominent the mean presentation of the organization's ROA, the better benefit of the organization, on the grounds that the pace of return progressively producing benefits versus the somewhat little resources (Kim and Kim 2010) as cited by

| [27] | Akinroluyo, B. I., & Adeoti, J. (2022). CAPITAL ADEQUACY AND DEPOSIT MONEY BANK'S RETURN ON ASSET (ROA) IN NIGERIA. Finance & Accounting Research Journal, 4(1), 1-13. https://doi.org/10.51594/farj.v4i1.284 |

[27]

. Higher ROA esteem demonstrates better organization execution, due to better yield on venture rate. "This worth mirrors the organization's profit from all resources (or subsidizing) gave to the organization" (Wild, 2005) as cited by

| [27] | Akinroluyo, B. I., & Adeoti, J. (2022). CAPITAL ADEQUACY AND DEPOSIT MONEY BANK'S RETURN ON ASSET (ROA) IN NIGERIA. Finance & Accounting Research Journal, 4(1), 1-13. https://doi.org/10.51594/farj.v4i1.284 |

[27]

.

Several earlier authors have used several formulas in calculating ROA as indicated below:

ROA = Net Income / Total Assets * 100% (Tandelilin, 2010) as cited by

| [28] | Setiawan, A., & Sumantri, M. (2020). The Effect of Return On Asset (ROA), Debt to Equity Ratio (DER), and Earning Per Share (EPS) on Stock Prices in the Mining Sector on the Indonesia Stock Exchange for the 2015 - 2019 Period. Technium, 2(7), 324-335. |

[28]

.

ROA = Earnings before Tax / Average of Total Assets

| [23] | Usy, K., Sulaeman, R., Aldrin, H., & Rachmat, S. (2020). Financial Performance and Macroeconomics toward Capital Adequacy: Empirical Evidence from Indonesian Banking. International Journal of Innovation, Creativity and Change, 12(12), 661-674. |

[23]

.

ROA = 100% x Earnings before Tax Total Assets Average

| [29] | Bambang, W., & Chalimatuz, S. (2022). FINANCIAL DISTRESS, DIVIDEND POLICY, RGEC AND EARNING PER SHARE. Trikonomika, 21(1), 37-45. |

[29]

.

ROA = Net Income available to Stockholders / Total Assets X 100

| [3] | Wahyuni, P., & Umam, D. (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12-28. https://doi.org/10.51505/IJEBMR.2023.7602 |

[3]

.

ROA = Available net profit for common shareholders / Total assets

| [27] | Akinroluyo, B. I., & Adeoti, J. (2022). CAPITAL ADEQUACY AND DEPOSIT MONEY BANK'S RETURN ON ASSET (ROA) IN NIGERIA. Finance & Accounting Research Journal, 4(1), 1-13. https://doi.org/10.51594/farj.v4i1.284 |

[27]

.

Return on Assets (ROA) = Net Profit before Tax/ Total assets

| [25] | Rafique, A., Quddoos, M., Akhtar, M., & Karim, A. (2020). Impact of Financial Risk on Financial Performance of Banks in Pakistan; the Mediating Role of Capital Adequacy Ratio. Journal of Accounting and Finance in Emerging Economies, 6(2), 607-613. |

[25]

.

In this study, ROA is defined as the ratio of Net Income to Total Assets and calculated as Net Income divided by Average Total Assets; thus:

“Return on Assets (ROA) = (Net Income / Average Total Assets)”.

Some of the previous authors that have made use of ROA as a dependent variable in their studies are:

| [53] | Agustina, Y., Winarno, A., & Dyan, A. (2021). Good Corporate Governance and Financial Performance on Capital Adequacy Ratio: A Reflection of Indonesian Conventional Banking. JBMP: Jurnal Bisnis, Manajemen dan Perbankan, 7(2), 293-306. https://doi.org/10.21070/jbmp.v7vi2.1542 |

| [54] | Mujtaba, G., Akhtar, Y., Ashfaq, S., Jadoon, I., & Hina, S. (2021). The nexus between Basel capital requirements, risk-taking and profitability: what about emerging economies? ECONOMIC RESEARCH-EKONOMSKA ISTRAŽIVANJA, 1-22. https://doi.org/10.1080/1331677X.2021.1890177 |

| [58] | Intonti, M., Ceo, A., & Ferri, G. (2022). Capital adequacy in banks and sustainable finance: the Green Supporting Factor. RISK MANAGEMENT MAGAZINE, 17(1), 50-61. |

[53-54, 58]

.

2.1.3. Capital Adequacy

Lekaaso et al. (2020) as cited by

| [9] | Ogunode, O. A., Awoniyi, O. A., & Ajibade, A. T. (2022). Capital adequacy and corporate performance of non-financial firms: Empirical evidence from Nigeria. Cogent Business & Management, 9(1), 1-16. https://doi.org/10.1080/23311975.2022.2156089 |

[9]

defined Capital adequacy as “sufficiency of capital for operational existence. Capital adequacy is essential for the soundness and economic performance of any organization; however, the argument that is still open ended is determining how much capital is adequate to drive business success”. Capital sufficiency acts “as a safety net in case of any unforeseen circumstances. Its high ratio suggests less external financing, which results in higher profitability”

| [32] | Mulyanto, N., Donny, A., & Abdul, H. (2021). The effect of loan-loss provision, non-performing loans and third-party fund on capital adequacy ratio. Accounting, 7, 943-950. https://doi.org/10.5267/j.ac.2021.1.013 |

[32]

. He further stated that “the goal of the capital adequacy criterion is to guarantee that each financial institution that accepts deposits maintains an adequate amount of capital to guard or cushion customers’ deposits against losses brought on by business risks that financial institutions encounter. The risks listed here include those related to credit, investments, legislation, liquidity, interest rates, and competition”.

The capital which “banks hold with themselves as required by financial regulator is known as minimum capital requirement. Banks exposed to various types of risks while granting loans and advances to various sectors. In order to absorb any losses which banks face from its business, it is imperative that banks should have sufficient capital. If banks have adequate capital, then it can protect its depositors from unforeseen contingencies as well promotes the stability and efficiency of financial systems”

| [30] | Nikhat, F. (2014). Capital Adequacy: A Financial Soundness Indicator for Banks. Global Journal of Finance and Management, 6(8), 771-776. |

[30]

.

In Nigeria, Central bank of Nigeria (CBN) has issued a circular on the review of the minimum capital requirements for Commercial, Merchant, and Non-Interest Banks in Nigeria due to the prevailing macroeconomic challenges and headwinds occasioned by external and domestic shocks facing all banks globally and in Nigeria in particular. The regulator in line with section 9 of the Banks and Other Financial Institution Act (BOFIA), 2020 has announced the upward review of minimum capital requirements for commercial, merchant and non-interest banks in Nigeria as follows:

Effective March 31, 2026; Minimum Capital of Commercial banks with International, National and Regional authorizations should be N500 billion; N200 billion and N50 billion respectively. Merchant Banks minimum capital was increased to N20 billion while Non-Interest banks with National and Regional authorization were also increased to N20 billion and N10 billion respectively. All banks should ensure that the new minimum capitals comprise of only paid-up capital and share premium only without retained earnings or not based on Shareholders’ Fund

.

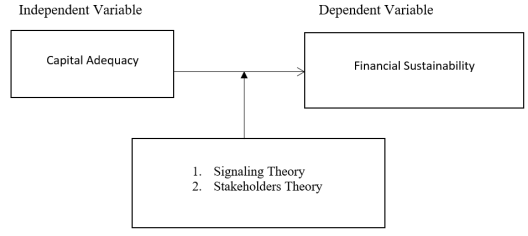

2.2. Theoretical Framework

This study was anchored mainly on Stakeholders Theory and Signaling Theory.

2.2.1. Stakeholder Theory

This theory was first prescribed in 1983 by Dr. F. Edward Freeman. It suggests that shareholders are merely one of the many stakeholders in a company. Freeman and Reed (1983) distinguished two classes of stakeholders; “The narrow definition of stakeholder include those groups who are vital to the survival and success of the corporation while the wide definition includes any group or individual who can affect or is affected by the company”

| [33] | Freeman, R. E., & Reed, D. L. (1983). Stockholders and Stakeholders: a new perspective on corporate governance. Sagepub. Retrieved from https://journals.sagepub.com |

[33]

. Typical stakeholders are owners/shareholders, employees, creditors/suppliers, customers, management, community, government and trade association. The theory suggests that every organization strives to create value for all stakeholders as a reason for its existence. In addition to fulfilling its economic responsibilities to the shareholders, the firm is obligated to fulfill the legal and ethical responsibility to society, the government and customers in order to attain sustainable long – term value for the organization. Failure to accomplish these responsibilities can cause failure in the value creation process for organization

| [34] | Parveneh, S., Saudah, S., & Siti, Z. B. (2014). A PROPOSED MODEL OF THE RELATIONSHIP BETWEEN ENTERPRISE RISK MANAGEMENT AND FIRM PERFORMANCE. INTERNATIONAL JOURNAL OF INFORMATION PROCESSING AND MANAGEMENT, 70-80. |

[34]

.

Fostering positive connections with key stakeholders help improve the performance of the firm and its value. Stakeholder relationships and resource allocation decisions are inseparable, because managers distribute resources according to the strength of stakeholder relationships and these set of variables interact to affect firm value

| [35] | Dyreng, S., Hanlon, M., & Maydew, E. (2009). The effects of managers on corporate tax avoidance. USA: Duke University, University of Michigan, University of Carolina. |

[35]

. The sustainability of deposit money banks depends on the survival of their managements. According to

| [36] | Pandey, I. M. (2008). Financial Management. New Delhi: Vikas Publishing House (PVT) Ltd. |

[36]

; he noted managers can survive only when they are successful; and they are successful only when they manage the company better than someone else. The theory was however criticized for its limited usefulness as an oversimplified theory, considering the efficient markets hypothesis, which is foundational to the field of finance. The theory is relevant to this study because all the parties involved in capital raising process; ranging from managers, investors, customers, regulators are all stakeholders.

Figure 1. Theoretical Framework.

2.2.2. The Signaling Theory

The theory was propounded by Spence in 1973 and the concern of the theory is to fundamentally reduce the information asymmetry between two parties. “Signaling theory is useful for describing behavior when two parties (individuals or organizations) have access to different information. Typically, one party, the sender, must choose whether and how to communicate (or signal) that information, and the other party, the receiver, must choose how to interpret the signal. Accordingly, signaling theory holds a prominent position in a variety of management literatures, including strategic management, entrepreneurship, and human resource management”

. In formulating the signaling theory,

| [38] | Spence, M. (1973). Job Market Signaling. Quarterly Journal of Economics, 87(3), 355-374. |

[38]

utilized the labor market to model the signaling function of education. He stated that “some potential employers lack information about the quality of job candidates. The candidates, therefore, obtain education to signal their quality and reduce information asymmetries. This is presumably a reliable signal because lower quality candidates would not be able to withstand the rigors of higher education”. Other earlier supporters of the theory along Spence (1973) are: Bird and Smith (2005); Zhang and Wiersema (2009); Miller and Triana (2009).

The theory is related to this study because management must communicate to the potential investors the reasons why they should invest in their companies or reasons why investing in firm A is better than firm B in providing the buffer capital required.

2.3. Empirical Review

Several authors have dealt with capital adequacy and financial sustainability. This study conducted the review of the related past studies in line with the formulated specific objectives in this section.

2.3.1. Capital Adequacy and Return on Equity

The following earlier studies used ROE as one of their dependent variables to measure financial performance and concluded on a positive association between capital adequacy and financial performance.

Kong et al. (2023) examined “Capital Structure and Corporates Financial Sustainability: Evidence from Listed Non-Financial Entities in Ghana” and concluded that Capital Structures, Firms’ sizes and Assets Growth improved the financial performance

| [20] | Kong, Y., Donkor, M., Musah, M., Nkyi, J. A., & Ampong, G. O. (2023). Capital Structure and Corporates Financial Sustainability: Evidence from Listed Non-Financial Entities in Ghana. Sustainability MDPI, 15(4211), 1-20. https://doi.org/10.3390/su15054211 |

[20]

. The study on “A Performance of Capital Adequacy Ratio Indicator in Private Sector Banks – An Empirical Study” by

also concluded among others that CAMEL play significant roles in ROA, Equity and Investment Decisions of investigated banks. In the same manner, Aliyu et al. (2023) concluded that the CBN Minimum Capital Requirement (CR) has a significant impact on the financial sustainability of MFIs during their review of “Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria”

| [5] | Aliyu, A., Gambo, N., Enesi, O. E., & Ibrahim, M. (2023). Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria. European Journal of Accounting, Auditing and Finance Research, 11(10), 73-97. https://doi.org/10.37745/ejaafr.2013/vol11n107397 |

[5]

. Ogunode et al. (2022) concluded in the study titled “Capital adequacy and corporate performance of non-financial firms: Empirical evidence from Nigeria” that firm sizes and profitable use of debt in capital mix are key factors that can “positively drive corporate performance”

| [9] | Ogunode, O. A., Awoniyi, O. A., & Ajibade, A. T. (2022). Capital adequacy and corporate performance of non-financial firms: Empirical evidence from Nigeria. Cogent Business & Management, 9(1), 1-16. https://doi.org/10.1080/23311975.2022.2156089 |

[9]

.

Al-Sharkas and Al-Sharkas (2022), in a similar vein examined “the Impact on Bank Profitability: Testing for Capital Adequacy Ratio, Cost Income Ratio and Non-Performing Loans in Emerging Markets” and concluded that the impact of banks’ profitability differs based on the proxy used for Capital Adequacy

| [39] | Al-Sharkas, A., & Al-Sharkas, T. (2022). THE IMPACT ON BANK PROFITABILITY: TESTING FOR CAPITAL ADEQUACY RATIO, COST-INCOME RATIO AND NON-PERFORMING LOANS IN EMERGING MARKETS. Journal of Governance and Regulation, 11(1), 231-243. https://doi.org/10.22495/jgrv11i1siart4 |

[39]

. The study confirmed that while ROA was negatively correlated with CA, ROE on the hand was positively affected by CA. Marta et al. (2022) concluded that both ROA and ROE have a positive effect on EP; which means the higher the ratio of assets and the ratio of capital owned by Islamic banking the higher the profit sharing level of Islamic banking; while examining the interactive effect of Capital Structure on Profitability and Earnings Per Share of Sharia Bank

| [16] | Marta, M. S., Gunawan, A., Maesaroh, S. S., Nugraha, & Bahri, S. (2022). Interactive Effect of Capital Structure on Profitability and Earning Per Share of Sharia Bank. Journal of Islamic Economics and Business, 2(2), 97-111. |

[16]

.

Efuntade et al. (2019) concluded their study titled “Capital Structure and Earnings per Share in Listed Conglomerates in Nigeria” that a well configured capital structure management function plays a significant role on the firms’ profitability levels

| [14] | Efuntade, A. O., Efuntade, O. O., & Akinola, A. O. (2019). Capital Structure and Earnings per Shares in Listed Conglomerates in Nigeria. European Journal of Accounting, Auditing and Finance Research, 7(8), 49 - 58. |

[14]

. Capital structure is confirmed to have positively affected and significantly improved the firms’ performances in terms of profitability and size of firms in Nigeria. In a similar study of “Capital Adequacy, Asset Quality and Banking Sector Performance” by

| [55] | Ikpesu, F., & Oke, B. (2022). Capital Adequacy, Asset Quality and Banking Sector Performance. ACTA UNIVERSITATIS DANUBIUS, 18(3), 22-32. |

[55]

; it was concluded that adequate capital and sound assets quality result in improved earnings and performances for banks. The study of “Profitability and Financial Sustainability of Microfinance Banks in Nigeria” by

| [4] | Gambo, N., Rikwentishe, R., Usman, N. D., & Ikyabo, A. Y. (2022). PROFITABILITY AND FINANCIAL SUSTAINABILITY OF MICROFINANCE BANKS IN NIGERIA. FUW-INTERNATIONAL JOURNAL OF MANAGEMENT AND SOCIAL SCIENCES, 7(2), 1-21. |

[4]

revealed that size of microfinance institution influences profitability; the capital and deposit base ratios influence also influence profitability. Liu and Huang (2022) examined the “Sustainable Financing and Financial Risk management of Financial Institutions – Case Study on Chinese Banks” and confirmed that “positive shock of risk management positively impacted the sustainable financing”

| [56] | Liu, H., & Huang, W. (2022). Sustainable Financing and Financial Risk Management of Financial Institutions—Case Study on Chinese Banks. Sustainability, 14, 1-18. https://doi.org/10.3390/su14159786 |

[56]

.

However and contrary to the above positive positions by some previous researchers, the following research works concluded on a negative association between Capital Adequacy and ROE as Financial Sustainability variable: Mauldha and Kusumah (2023) concluded on “a study of the impact of psak 71 implementation on financial performance and capital adequacy ratio” that Application of PSAK 71 does not have impact on the achievement of profit/loss that may affect the capital. The study concluded that “PSAK71 has a significant effect on ROA and DER but not on ROE and LDR. Therefore, its application has no significant effect on minimum capital adequacy requirements”

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

[17]

. Balami and Chalise (2023) also concluded on a negative note during their study on Capital Adequacy and its Influence on Bank Profitability in Nepal. The study revealed that a complex relationships were established and consequently there exist significantly negative correlations between ROA, ROE and Capital and also positively insignificant relationship between Government Securities, Total Investments and Profitability. The study concluded that CA had insignificant effect on ROA

| [40] | Balami, S., & Chalise, D. R. (2023). Capital Adequacy and its Influence on Bank Profitability in Nepal. International Journal of Silkroad Institute of Research and Training (IJSIRT), 1(2), 106-114. https://doi.org/10.3126/ijsirt.v1i2.61771 |

[40]

.

The specific objective of this section of the empirical review is to evaluate the effect of capital adequacy on return on equity of listed deposit money banks in sub-Sahara African countries. Some of the gaps identified for this study are limited data subject to their non-availability; non-disclosure of sampling size and techniques adopted in determining the sizes; restriction of the scope of the study to a country like Nigeria or Ghana only; non-disclosure of the scope of the studies; non-alignment of recommendations and objectives of the studies. Instances noted where there was no evidence of empirical review or using of a single market like Jordan market to represent the whole emerging markets.

2.3.2. Capital Adequacy and Return on Assets

The following prior studies used ROA as a dependent variable in measuring financial performances and concluded on positive association between capital adequacy and financial sustainability.

Sridevi et al. (2023) concluded that CAMEL play significant roles in ROA, Equity and Investment Decisions during their study of “A Performance Of Capital Adequacy Ratio Indicator In Private Sector Banks - An Empirical Study"

. Similarly, Mauldha and Kusumah (2023) concluded that PSAK 71 has a significant effect on ROA and DER as an outcome of their study on “A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio”

| [17] | Mauldha, V. E., & Kusumah, R. R. (2023). A Study of the Impact of PSAK 71 Implementation on Financial Performance and Capital Adequacy Ratio. WIGA: Jurnal Penelitian Ilmu Ekonomi, 13(1), 74-83. https://doi.org/10.30741 |

[17]

. Aliyu et al. (2023) also concluded during the study of “Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria” that CBN Minimum Capital Requirement has a significant impact on the financial sustainability of MFIs

| [5] | Aliyu, A., Gambo, N., Enesi, O. E., & Ibrahim, M. (2023). Central Bank Regulations and the Financial Sustainability of National Microfinance Banks in Nigeria. European Journal of Accounting, Auditing and Finance Research, 11(10), 73-97. https://doi.org/10.37745/ejaafr.2013/vol11n107397 |

[5]

. A study conducted by

| [41] | Duho, K. C. (2023). Determinants of capital adequacy and voluntary capital buffer among microfinance institutions in an emerging market. Cogent Economics & Finance, 11(2), 1-33. https://doi.org/10.1080/23322039.2023.2285142 |

[41]

on “Determinants of capital adequacy and voluntary capital buffer among microfinance institutions in an emerging market” concluded that “Credit Risk, Income Diversification, Size, Profitability, Lending Channel and Equity to Assets ratios significantly affected capital adequacy”.

Ezu et al. (2023) examined the “Effect of Capital Adequacy on the Performance of Deposit Money banks in Nigeria” and their findings revealed that all considered variables had direct and inverse linear significant effect on ROA. The study concluded that “Capital Adequacy has both direct and inverse linear relationship with efficient performance of banks”

| [42] | Ezu, G., Nwanna, I. O., & Eke-Jeff, O. M. (2023). Effect of capital Adequacy on the Performance of Deposit Money banks in Nigeria. International Journal of Novel Research in Marketing Management and Economics. 10(1), 53-63. https://doi.org/10.5281/zenodo.7774547 |

[42]

. A study conducted by

| [22] | Sapitri, N., & Irawan, B. (2023). Impact of the Capital Adequacy Ratio (CAR) and Mudharabah on the Return on Asset (ROA) on Sharia General Banks Registered in the Financial Services Authority (OJK). Journal of Waqf and Islamic Economic Philanthropy, 1(1), 1-12. |

[22]

on the “Impact of the Capital Adequacy Ratio (CAR) and Mudharabah on the Return on Asset (ROA) on Sharia General Banks Registered in the Financial Services Authority (OJK)” concluded that “there exist a positively statistically significant relationship between the Capital Adequacy Ratio (CAR) and Return on Assets (ROA) while the impact of Mudharabah was found to be insignificant on ROA of Islamic Commercial banks. However, combined effect of CAR and Mudharabah has a positive and significant relationship on ROA of Islamic Commercial Banks”.

In the same vein; Gambo et al. (2022) examined “Profitability and financial sustainability of Microfinance Banks in Nigeria” and concluded that size of microfinance institution influences profitability; the capital and deposit base ratios influence profitability

| [4] | Gambo, N., Rikwentishe, R., Usman, N. D., & Ikyabo, A. Y. (2022). PROFITABILITY AND FINANCIAL SUSTAINABILITY OF MICROFINANCE BANKS IN NIGERIA. FUW-INTERNATIONAL JOURNAL OF MANAGEMENT AND SOCIAL SCIENCES, 7(2), 1-21. |

[4]

. Rustam and Adil (2022) studied “Financial Sustainability Ratio and Aspects That Affect It” and the study concluded that “CAR, Company Size and LDR have a positively significant impact on financial sustainability while ROA had a negative and insignificant effect on the financial sustainability ratio”

. Marta et al. (2022) analyzed the “Interactive Effect of capital Structure on Profitability and Earnings per Share of Sharia Banks” and the study revealed that both ROA and ROE have a positive effect on EPS. This means that the higher the ratio of assets and the ratio of capital owned, the higher the profit sharing level in Islamic banking. However, further studies stated that DER weakens the relationship between ROA and ROE on EPS

| [16] | Marta, M. S., Gunawan, A., Maesaroh, S. S., Nugraha, & Bahri, S. (2022). Interactive Effect of Capital Structure on Profitability and Earning Per Share of Sharia Bank. Journal of Islamic Economics and Business, 2(2), 97-111. |

[16]

.

In 2021, various studies were conducted relating to the above positive positions. Arini and Titis (2021) examined “Factors Influence Financial Sustainability Banking in Indonesia” and concluded that three out of four financial performance factors / variables namely; ROA, LTA and DTA affect financial sustainability

| [12] | Arini, M., & Titis M. (2021). Factors Influence Financial Sustainability Banking in Indonesia. Al-Tijary Jurnal Ekonomi dan Bisnis Islam, 6(1), 41-50. https://doi.org/10.21093/at.v6i1.2497 |

[12]

. Similarly, Nguyen (2021) researched on “Capital adequacy ratio and a bank’s financial stability in Vietnam”. The research confirmed the existence of a positive correlation between CA and Financial Stability

. The study on “Sensitivity of Capital Adequacy Ratio to Bank – Specific and Economic Factors in the Arab Banking Sector” by

| [32] | Mulyanto, N., Donny, A., & Abdul, H. (2021). The effect of loan-loss provision, non-performing loans and third-party fund on capital adequacy ratio. Accounting, 7, 943-950. https://doi.org/10.5267/j.ac.2021.1.013 |

[32]

concluded that “CAR responds significantly and positively to the fluctuation in the size, the NPL, the ROA and the real GDP growth rate. However, growth of provisions has no significant effect on the CAR of Banks in Arab”.

However, few of the literatures reviewed did not agree with the above positive position and concluded on a negative association between the Capital Adequacy and ROA. The authors are: Balami and Chalise (2023) concluded in the study of “Capital Adequacy and its influence on Bank Profitability in Nepal” that there exist a significantly negative correlations between ROA, ROE and Capital and also positively insignificant relationship between Government Securities, Total Investments and Profitability and that CAR had insignificant effect on ROA

| [40] | Balami, S., & Chalise, D. R. (2023). Capital Adequacy and its Influence on Bank Profitability in Nepal. International Journal of Silkroad Institute of Research and Training (IJSIRT), 1(2), 106-114. https://doi.org/10.3126/ijsirt.v1i2.61771 |

[40]

. In the same vein, Wahyuni and Umam (2023) examined “The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach” and concluded that Credit Risk and Capital Adequacy effect on ROA are not significant while Operational Efficiency has a significant effect on ROA

| [3] | Wahyuni, P., & Umam, D. (2023). The Effect of Credit Risk, Capital Adequacy and Operational Efficiency on Banking Financial Performance with a Profitability Approach. International Journal of Economics, Business and Management Research, 7(6), 12-28. https://doi.org/10.51505/IJEBMR.2023.7602 |

[3]

. The findings on “The Impact of bank Profitability: Testing for Capital Adequacy Ratio, Cost-Income Ratio and non-Performing Loans in Emerging Markets” show that ROA is negatively correlated with CAR

| [39] | Al-Sharkas, A., & Al-Sharkas, T. (2022). THE IMPACT ON BANK PROFITABILITY: TESTING FOR CAPITAL ADEQUACY RATIO, COST-INCOME RATIO AND NON-PERFORMING LOANS IN EMERGING MARKETS. Journal of Governance and Regulation, 11(1), 231-243. https://doi.org/10.22495/jgrv11i1siart4 |

[39]

.

Some of the following authors have mixed conclusion on the relation of Capital Adequacy and ROA. Miranti (2023) studied “Effect of Capital Structure on Financial Sustainability of Sharia Public Financing Bank (BPRS)” and his findings revealed that Capital structure of banks had both direct and indirect effect on the financial sustainability of a BPRS. Thus, the capital structure has a more significant influence on the financial sustainability of the BPRS if the ROA value is included in the BPRS finances

| [26] | Titis Miranti, U. (2023). Effect of Capital Structure on Financial Sustainability of Sharia Public Financing Bank (BPRS). Ad-Deenar: Jurnal Ekonomi dan Bisnis Islam, 6(1), 137-152. https://doi.org/10.30868/ad.v6i01.2301 |

[26]

. ROA was able to mediate the effect of capital structure on their Financial Sustainability. The findings of

| [53] | Agustina, Y., Winarno, A., & Dyan, A. (2021). Good Corporate Governance and Financial Performance on Capital Adequacy Ratio: A Reflection of Indonesian Conventional Banking. JBMP: Jurnal Bisnis, Manajemen dan Perbankan, 7(2), 293-306. https://doi.org/10.21070/jbmp.v7vi2.1542 |

[53]

in their study of “Good Corporate Governance and Financial Performance on Capital Adequacy Ratio: A Reflection of Indonesian Conventional Banking” revealed that LDR, ROA, NPL and GCG had no impact on CAR because all their revenues were used to mitigate operational risk without any effect on CAR.

The objective of this section of empirical review is to determine the effect of capital adequacy on return on assets of listed DMBs in selected SSACs. Some of the identified gaps for this study are: non-disclosure of sampling techniques; non-alignment of objectives of the studies and the recommendations; theoretical framework not specified in some studies empirically studied; effect of mudharabah was found to be insignificant on ROA; instances were also observed where some variables have both direct and inverse linear relationship with ROA; limiting of scope to either country or sectorial specific; insufficient observation as a result of limited years of study; Data limitation; high processing error rates; non-accounting for country specific issues; non-disclosure of studies populations and incomprehensive scope of both internal and external factors.

4. Data Analysis, Results and Discussion of Findings

In this research work, the evaluation of the impact of capital adequacy and financial performance of listed deposit money banks in selected sub-Sahara African countries was done empirically with analysis and interpretation of data examined. The study consists of data extracted from the annual statements and accounts of 34 listed DMBs from the selected SSACs for the period 2014-2023. Find below the results of the data analyzed and its discussion:

4.1. Descriptive Analysis

Table 1. Summary of Descriptive Statistics.

Variable | Mean | Std. Dev | Min | Max |

ROE | 0.168 | 0.304 | -1.52 | 4.76 |

ROA | 0.0207 | 0.019 | -0.10 | 0.10 |

DTA | 0.652 | 0.166 | -0.05 | 1.61 |

LTA | 0.458 | 0.191 | 0.00 | 1.68 |

LLPTA | -0.614 | 3.762 | -50.065 | 2.503 |

ETL | 0.213 | 1.171 | -0.68 | 21.6 |

Source: Researcher’s Computation, 2025 (Excerpts from Stata 12.0 1C Output)

Where “ROE indicates Return on equity, ROA – Return on assets, DTA – Deposit to Total Assets, LTA – Loan to Total Assets, LLPTA – Loan Loss Provision to Total Assets, ETL – Equity to Total Liabilities, Std. Dev – Standard deviation, Min – Minimum, Max - Maximum”.

Table 1 summarized the descriptive statistics for the variables used in the study with key statistics such as the mean, standard deviation, minimum, and maximum values. These statistics help to understand the data's central tendency, dispersion, and range. The Return on Equity (ROE) has a mean value of 0.168, which suggests that, on average, firms generate a 16.8% return on their equity. The standard deviation of 0.304 means considerable variability among firms with ROE values ranging from a minimum of -1.52, indicating losses, to a maximum of 4.76, representing exceptional returns. Within the period of this study, the least loss reported was -1.52 on every unit of Total equity which implies capital depreciation to the shareholders. However, a maximum value of 4.7 indicates that the banks were able to generate a return of 4.76 on every unit of Total equity within the period under the study. Similarly, the Return on Assets (ROA) has a mean value of 0.0207, implying that firms earn an average return of 2.07% on their assets. The standard deviation of 0.019 suggests relatively low variation, with ROA values between -0.1 and 0.1, reflecting consistent firm performance.

The Deposit to Total Assets Ratio (DTA) has a mean of 0.652, which means that firms generally finance approximately 65.2% of their assets through debt. The standard deviation of 0.166 means moderate variability, with DTA values spanning from -0.05, indicating a negative relationship, to 1.61, suggesting high debt reliance. The Loan to Total Assets Ratio (LTA) has a mean of 0.458, showing that, on average, 45.8% of a firm's assets are financed through loans. The standard deviation of 0.191 and a range of 0 to 1.68 indicate variability in firms' reliance on loans to fund their assets. The Loan Loss Provision to Total Assets Ratio (LLPTA) has an average value of -0.614, which is a low level of loan loss provisions compared to total assets. However, the high standard deviation of 3.762 and a wide range from -50.065 to 2.503 points to the wide disparities in provisioning strategies. Lastly, the Equity to Total Liabilities Ratio (ETL) has a mean of 0.213, indicating that firms, on average, generate earnings sufficient to cover 21.3% of their total liabilities. The standard deviation of 1.171 and a range from -0.68 to 21.6 demonstrate considerable variability in firms’ ability to manage liabilities through equity.

Table 2. Correlation Table and Variance Inflation Factor Test (Multi-collinearity Test).

| DTA | LTA | LLPTA | ETL | VIF | 1/VIF |

DTA | 1.0000 | | | | 1.14 | 0.874312 |

LTA | 0.3535 | 1.0000 | | | 1.14 | 0.874060 |

LLPTA | 0.0025 | 0.0301 | 1.0000 | | 1.00 | 0.998908 |

ETL | -0.0250 | 0.0037 | 0.0108 | 1.0000 | 1.00 | 0.999090 |

Average | 1.07 | |

Source: Researcher’s Computation, 2025

Table 2 evaluates the relationships between variables and checks for multi-collinearity issues. The correlation coefficients reveal the strength of associations between pairs of variables. For instance, debt-to-total asset ratio is positive but weakly associated with total loan to total asset ratio and LLPTA ratio, which implies that these three ratios move in the same direction as DTA increases or decreases; LTA and LLPTA increase or decrease as well. In contrast, DTA has a weak negative correlation with equity to total liability ratio indicating that there exist an inverse relationship between DTA and ETL.

Loan to total asset ratio is positive but also weakly associated with LLPTA and equity to total liabilities which implies that the three ratios move in the same direction as LTA increases or decreases; both LLPTA and ETL increase or decrease as well. Loan loss provision to total asset is positively associated with equity to total liabilities. Both LLPTA and ETL always move in the same direction according to this study. Whenever LLPTA increases or decreases, ETL also increases or decreases.

Multi-collinearity Test

The VIF values assess multi-collinearity, which arises when independent variables are highly correlated, leading to unreliable statistical outcomes. In this case, the highest VIF is 1.14, considered low and indicates no multi-collinearity among the variables. All VIF values for each of the Independent variables are below 10, confirming that multi-collinearity is not a concern in this model. The reciprocal of the VIF, known as 1/VIF, is provided as an additional check. The 1/VIF values are all close to 1 to further support the conclusion that multi-collinearity is not an issue in this dataset.

4.2. Regression Analyses / Test of Hypotheses

Research Objective One: Evaluate the effect of capital adequacy on return on equity of listed deposit money banks in selected sub-Sahara African Countries.

Research Question One: What is the effect of Capital Adequacy on Return on Equity of Listed Deposit Money banks in selected sub-Sahara African Countries?

Research Hypothesis One (H01): Capital Adequacy has no significant effect on Return on Equity of Listed Deposit Money banks in selected sub-Sahara African Countries.

Table 3. Test of Hypothesis One.

Pooled Ordinary Least Square Regression Analysis with Robust Standard Error |

Variable | Coeff | Std. Err | T-Stat | Prob |

DTA | 0.015 | 0.096 | 0.16 | 0.876 |

LTA | -0.118 | 0.0939 | -1.26 | 0.208 |

LLPTA | 0.004 | 0.0009 | 4.31 | 0.000 |

ETL | -0.008 | 0.0025 | -3.31 | 0.001 |

Constant | 0.217 | 0.052 | 4.16 | 0.000 |

Adj.R2 | 0.0086 |

F-Stat/Wald Stat (Prob) | 43.81 (0.0000) |

Hausman Test | Chi2(2) = 0.99 (0.9115) |

LM Test | Chi2(1) = 0.00 (1.000) |

Heteroskedasticity Test | Chi2(13) = 96.01 (0.000) |

Autocorrelation Test | F (1, 19) = 1.650 (0.2079) |

Cross section independence test | 0.352 (0.7251) |

Source: Researcher’s Computation, 2025 (Excerpts from Stata 12.0 IC Output).

Dependent Variable: ROE @ 0.05 significance level.

The Hausman test, alongside its confirmatory checks (Testparm and Lagrangian Multiplier tests), was utilized to identify the most appropriate estimation method among Random Effects, Fixed Effects, and Pooled Ordinary Least Squares (OLS). The null hypothesis of the Hausman test favors Random Effects, and the high p-value (0.9115) indicates the null cannot be rejected, suggesting Random Effects is suitable. However, the LM result (p-value = 1.000) conflicts with this outcome, thus supports the appropriateness of Pooled Ordinary Least Square over Random Effects. Consequently, Pooled Ordinary Least Square was employed for the final regression. Diagnostic checks were performed to confirm the robustness of the model. The heteroskedasticity test yielded a significant p-value (0.000), suggesting the presence of non-constant variance in the residuals. Thus, the null hypothesis of homoskedasticity was rejected. The Wooldridge test for autocorrelation resulted in a p-value of 0.208, signifying no serial correlation among the residuals and model coefficients. Robust standard errors were applied to the regression analysis to address heteroskedasticity.

Regression Equation Results

(5)

(6)

From the result of the analysis presented in

Table 3, the regression analysis of the effect of Capital Adequacy (DTA, LTA, LLPTA, ETL) affect Returns on Equity (ROE). The probability of the T-test was used in determining the statistical significance of the effect of each proxy of Capital Adequacy (CA) on Returns on Equity (ROE) of the selected banks at 5% significance level. The result shows that, ETL and LLPTA have p-values of 0.001 and 0.000 respectively, which is less than 5%, while DTA and LTA have probability values of 0.876 and 0.208 respectively, which is greater than 5%. This implies that ETL and LLPTA have a significant effect on ROE, while DTA and LTA do not significantly affect ROE at 5 percent level of significance.

The proportion and direction of the effect of each independent variable’s proxies were estimated using both the signs and estimates of the coefficient. The results indicate that two of the proxies of Capital Adequacy (CA) (that is, LTA and ETL) have negative effects on the Returns on Equity (ROE), with coefficient values of -0.118 and -0.008, respectively; while the other two sub-variables (DTA and LLPTA) have positive effects (0.015 and 0.004) on ROE respectively. This means that as LTA and ETL increase by 1 percent, there would be a decrease in the Returns on Equity (ROE) of the selected banks by 11% and 0.8%, respectively. Likewise, as DTA and LLPTA increase by 1%, there would be a corresponding increase in ROE by 1.5% and 0.4% respectively.

The result of the adjusted R2, which measured the magnitude of change caused on ROE by the combination of the interactions between the proxies of Capital Adequacy (CA), reveals that about 0.9% of the variation in ROE is caused by the joint interaction of the Capital Adequacy (CA)’s sub-variables adopted for this study, while the other 99.1% change in the ROE was caused by other factors not included in this study (macroeconomic variables such as interest rates, inflation, and exchange rate volatility and internal factors such as managerial efficiency, technological adoption, and customer relationship management are other factors not captured).

Decision

At a level of significance 0.05 and degree of freedom 4, 302; the F-statistics is 43.81, while the p-value of the F-statistics is 0.0000 which is less than the 0.05 adopted level of significance. Therefore, the study rejected the null hypothesis, which implied that Capital Adequacy has a statistical significant effect on ROE of Listed DMBs in selected SSACs. Therefore, the findings of this hypothesis confirmed that Capital Adequacy is statistically significant to the financial performance (ROE) of listed deposit money banks in the selected sub-Sahara African countries.

Discussion of Finding

This study confirm a “significant relationship between capital adequacy and the return on equity (ROE) of listed DMBs in selected SSACs”. The regression analysis demonstrated that while proxies of capital adequacy, like LLPTA and ETL, have significantly impact ROE, others, including DTA and LTA, do not exhibit statistical significance at the 5% level. These findings align with the theoretical underpinnings of capital adequacy, which suggest that its various dimensions may exert differential impacts on financial performance metrics depending on the operational context.

Specifically, the statistically significant positive effect of LLPTA on ROE supports the view that prudent loan loss provisioning can enhance banks' profitability by mitigating credit risk and ensuring financial stability. This outcome corroborates the findings of

| [42] | Ezu, G., Nwanna, I. O., & Eke-Jeff, O. M. (2023). Effect of capital Adequacy on the Performance of Deposit Money banks in Nigeria. International Journal of Novel Research in Marketing Management and Economics. 10(1), 53-63. https://doi.org/10.5281/zenodo.7774547 |

[42]

, who highlighted that effective credit risk management practices, particularly in developing economies, bolster profitability by safeguarding the quality of asset portfolios. Also, the significant but negative effect of ETL on ROE reflects the challenges associated with excessive leverage, which can increase financial distress risks and reduce profitability. This is consistent with the work of

| [44] | Sandow, J., Duodu, E., & Oteng-Abayie, E. (2021). Regulatory capital requirements and bank performance in Ghana: evidence from panel corrected standard error. Cogent Economics & Finance, 9, 1-16. https://doi.org/10.1080/23322039.2021.2003503 |

[44]

, who observed that highly leveraged banks in Ghana experienced diminished ROE due to increased cost pressures and vulnerability to economic shocks.

Moreover, the adjusted R² implies that only a small proportion of the variability in ROE is explained by the combined effects of the selected capital adequacy proxies, suggesting that other factors not included in this model play a more substantial role in driving profitability. This resonates with studies by

| [9] | Ogunode, O. A., Awoniyi, O. A., & Ajibade, A. T. (2022). Capital adequacy and corporate performance of non-financial firms: Empirical evidence from Nigeria. Cogent Business & Management, 9(1), 1-16. https://doi.org/10.1080/23311975.2022.2156089 |

[9]

, who emphasized that macroeconomic variables such as interest rates, inflation, and exchange rate volatility significantly influence bank performance in sub-Sahara Africa and internal factors such as managerial efficiency, technological adoption, and customer relationship management also contribute to financial performance, according to

| [45] | Mbaeri, M. N., Uwalake, U., & Gimba, J. T. (2021). Capital Adequacy Ratio and Financial Performance of Listed Commercial Banks in Nigeria. Journal of Economics and Allied Research, 6(3), 81-88. |

[45]

.

Research Objective Two: Determine the effect of CA on ROA of listed DMBs in selected SSACs.

Research Question Two: How does CA affect ROA of listed DMBs in selected SSACs?

Research Hypothesis Two (H02): There is no significant effect of CA on ROA of listed DMBs in selected SSACs.

Table 4. Test of Hypothesis Two.

Random-effects GLS regression |

Variable | Coeff | Std. Err | T-Stat | Prob |

DTA | -0.040 | 0.014 | -2.84 | 0.004 |

LTA | 0.021 | 0.0117 | 1.81 | 0.070 |

LLPTA | 0.004 | 0.00005 | 9.48 | 0.000 |

ETL | -0.0003 | 0.0003 | -0.73 | 0.465 |

Constant | 0.037 | 0.009 | 4.14 | 0.000 |

Adj.R2 | 0.1358 |

F-Stat/Wald Stat (Prob) | 154.00 (0.0000) |

Hausman Test | Chi2(2) = 6.62 (0.1571) |

LM Test | Chi2(1) = 225.41 (0.000) |

Heteroskedasticity Test | Chi2(13) = 22.49 (0.000) |

Autocorrelation Test | F (1, 33) = 2.196 (0.1478) |

Cross section independence test | 0.242 (0.6140) |

Source: Researcher’s Computation, 2025 (Excerpts from Stata 12.0 IC Output).

Dependent Variable: ROA @ 0.05 significance level.

In determining the appropriate estimating technique among Random effect, Fixed Effect, and Pooled Ordinary Least Square, the Hausman test, supported by LM (Lagrangian Multiplier test), were conducted. The null hypothesis of the Hausman test is that the preferred model is random effects, and the probability of the result (0.1571) suggests that the null hypothesis is not to be rejected. Thus, the preferred estimation method is random effect. However, the probability value of the confirmatory test (LM Test), which is 0.000, opposes the result of the Hausman test and suggests that Random-Effect Regression is not the best estimating technique for Model Two. Hence, the model was regressed adopting the pooled ordinary least square estimation. The heteroskedasticity test was then conducted to check for model residual variations. The probability value for the heteroskedasticity test result was 0.000, which implies that the model is not homoskedastic, meaning that the model does not have constant variance over time. Thus, the study rejects the null hypothesis. Also, the model coefficients and residuals were checked for autocorrelation problems using the Wooldridge test. With the probability value of 0.1478, it revealed that the model's coefficients and residuals are not correlated, and thus, there is no serial correlation problem in the model. The econometric issue (heteroskedasticity) observed in the model was thus addressed by running the regression with the robust standard errors option.

Regression Equation Results

(7)

(8)

The results of the regression analysis in

Table 4 showed that Capital Adequacy proxied by DTA, LTA, LLPTA, ETL affect ROA. The probability of the T-test was used in determining the statistical significance effect of each proxies of CA on the ROA of the selected banks at the 0.05 significance level. The results showed that DTA and LLPTA have probability values of 0.004 and 0.000, respectively, less than the adopted 0.05 significance level. In contrast, LTA and ETL have probability values of 0.070 and 0.465, respectively, greater than the adopted 0.05 level of significance. This means that DTA and LLPTA have a statistical significant effect on ROA, while LTA and ETL do not have a statistical significant effect on ROA at the significance level of 5 percent.

The magnitude and direction of the effect of each of the variable’s proxies were estimated using both the signs and estimates of the coefficients respectively. The results showed that two of the proxies of Capital Adequacy; DTA and ETL have negative effects on the ROA, with coefficient values of -0.040 and -0.0003, respectively; while the other two sub-variables (LTA and LLPTA) have positive effects (0.021 and 0.004) on ROA, respectively. This means that as DTA and ETL increase by 1 percent, there would be a decrease in the Return on Assets (ROA) of the selected banks by 4% and 0.03%, respectively. Likewise, as LTA and LLPTA increase by 1%, there would be a corresponding increase in ROA by 2.1% and 0.4%, respectively.

The adjusted R2 result, which measures the magnitude of change caused on ROA by the combination of the interactions between the proxies of Capital Adequacy (CA), means that about 13.58% of the variation in ROA was caused by the joint interaction of the Capital Adequacy (CA)’s sub-variables adopted for this study, while the other 86.42% change in the ROA was caused by other factors not included in this study.

Decision

At a 5 percent level of significance and degree of freedom 4, 302; the F- statistics is 154.00, while the p-value of the F-statistics is 0.0000 which is less than the adopted level of significance of 5 percent. Therefore, the study rejected the null hypothesis, which implied that CA has a statistical significant effect on the ROA of listed DMBs in the selected SSACs. Therefore, the findings of this hypothesis confirmed that Capital Adequacy is statistically significant to the financial performance (ROA) of listed deposit money banks in the selected sub-Sahara African countries.

Discussion of Findings

The study revealed the “relationship between CA and the ROA of listed DMBs in the selected SSACs. Through rigorous statistical analysis, it is established that certain proxies of Capital Adequacy exert significant effects on ROA, while others do not. Specifically, the results highlight the significant and negative effect of the DTA and the significant and positive effect of LLPTA on ROA. In contrast, the LTA and ETL demonstrated insignificant effects. These findings highlight the intricate dynamics of capital structure management and its implications for regional bank performance.

The negative effect DTA on ROA suggests that higher deposits relative to total assets could reduce asset profitability. This aligns with the findings of

| [46] | Olofin, A., Muritala, T., Maitala, F., Abubakar, H., & Ajalie, S. (2024). 9(6), e4777. https://doi.org/10.26668/businessreview/2024.v9i6.4777 |

[46]

, who argued that an over-reliance on deposits may increase liquidity risk and limit the efficient allocation of resources, thus reducing profitability. Similarly, Uremadu and Obim, (2024) found that while deposit mobilization is critical for banking operations, an excessively high DTA can signal underutilized funds or suboptimal asset allocation strategies, negatively impacting profitability

| [47] | Uremadu, S. O., & Obim, E. N. (2024). Effects of Deposit Mobilization on Financial Performance (Profitability) of Microfinance Banks in Nigeria. AKSU Journal of Administration and Corporate Governance, 4(1), 1-14. https://doi.org/10.61090/aksujacog.2024.001 |

[47]

. This is particularly pronounced in the sub-Sahara African banking contexts, where limited access to high-yield investment opportunities can exacerbate inefficiencies.

Conversely, the significant positive effect of LLPTA on ROA indicates that banks with prudent provisioning for loan losses tend to enhance their asset returns. This finding resonates with

| [48] | Maseke, B., & Swartz, E. (2021). Risk Management Impact on Non-Performing Loans and Profitability in the Namibian Banking Sector. Open Access Library Journal, 8(e6943). https://doi.org/10.4236/oalib.1106943 |

[48]

, who observed that effective loan loss provisioning serves as a risk management mechanism that not only safeguards banks from non-performing loans but also improves investor confidence, thereby contributing to profitability. Additionally, Gnan et al. (2023) highlighted that adequate provisioning can create a buffer against economic shocks, enabling banks to maintain steady returns, even in volatile environments